How to Monitor Your Financial Health

You don’t have to visit the doctor to figure out metrics like your height and weight. But your other vitals? That’s a different story. And what lurks beneath the surface might be hazardous to your future, without you knowing it.

If you’re young, high blood pressure and high cholesterol likely won’t hurt you in the short-term. But over the long-term, they become disastrous. They cause heart disease, strokes, and other cardiovascular diseases, which are leading causes of death in the US. Most are unexpected.

This is why getting a routine physical exam is so important. You learn if you are at risk for one of these silent killers, and you can create a plan for reducing your health risk.

You can do the same thing with your finances.

Your physical height and weight are kind of like your income and net worth. They are the big, top-line numbers you focus on to know how much money is coming in, and how much total wealth you’ve accumulated. They give a good indication of how healthy your finances are and you can figure them out quickly.

But there are three financial metrics you should be tracking that will help you reduce your risk of silent financial killers.

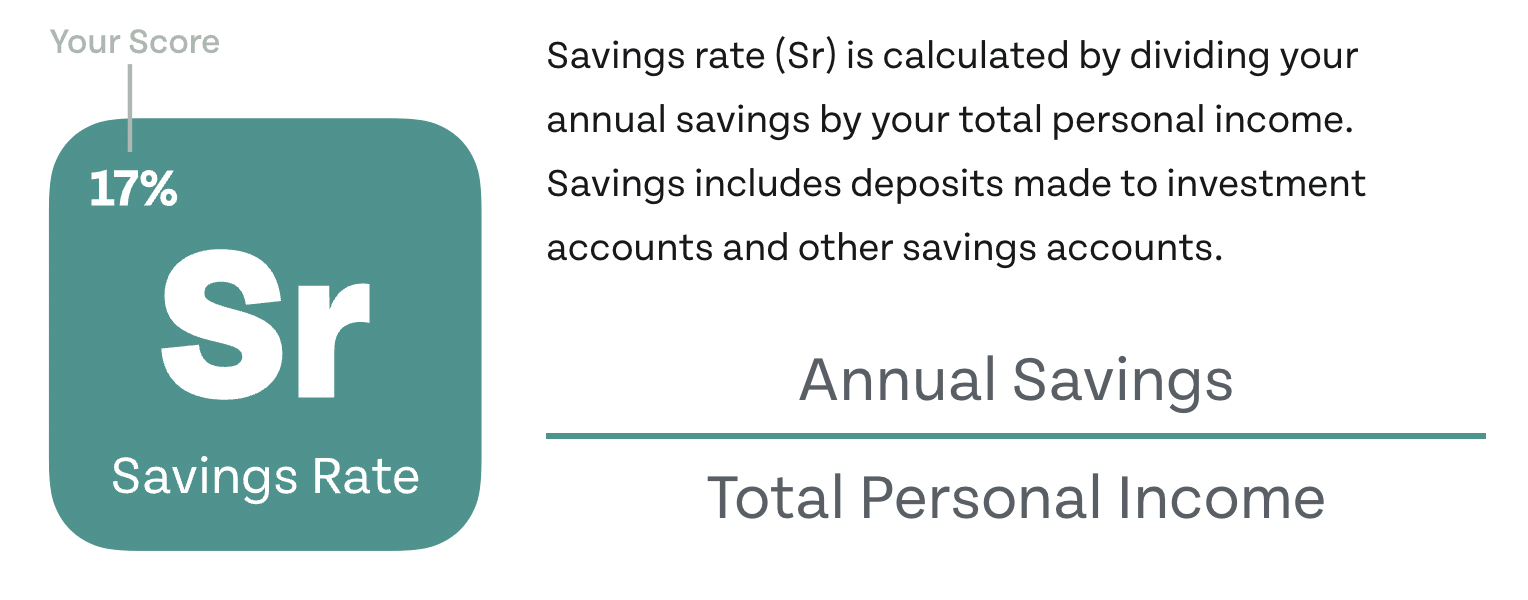

Savings Rate: How much of your income you are saving for the future.

Rule of Thumb: Savings Rate of 10% is good. Anything over 20% is excellent.

This is one of the best indicators for long-term financial success. Having a higher savings rate gives you more financial flexibility. This comes in handy if you have unexpected expenses like a car or medical bill. You can have a high income, but if you are not saving enough, you might be living paycheck to paycheck and feel more stressed about money.

Burn Rate: How much of your income you spend on personal expenses (excluding debt, savings and taxes).

Rule of Thumb: Burn Rate between 30-50% is considered normal. Over 50% is elevated.

Having an awareness of your spending habits is important because it affects how much you can save and pay off debt. If you have a high burn rate, it can hinder your ability to become financially secure. It affects how much insurance you should apply for and how risky your investments should be.

Debt Rate: How much of your income you are spending on paying off debt.

Rule of Thumb: Debt Rate below 36% for total debt and below 28% for all housing debt is good.

If too much of your income is tied up in paying off debt such as your mortgage, student loans, auto loans, etc., it affects your ability to save for the future and upgrade your lifestyle. If you don’t want to become “house poor”, keep this calculation in mind.

These financial metrics are key because you don’t see them in your paycheck or bank account. But they offer a lot in terms of showing you how financially healthy you really are beneath the surface. Knowing your scores can help you plan to reduce your future financial risk.

Just like you go for your annual physical exam to get your blood pressure and cholesterol levels checked, you should monitor your financial savings rate, burn rate, and debt rate.

For disclosure information, please visit the link here